Quick Start

How inflation silently erodes your money’s value.

Imagine putting $100 in a drawer.

You come back five years later and take it out. Same crisp bill. Same value on paper. But when you go to spend it, something’s changed. The $100 doesn’t buy what it used to.

Back then, you could buy two PS5 games at launch. Now that same $100 might barely cover one. Add tax, maybe a DLC, and you’re already short. That’s inflation. It doesn’t take your money. It takes what your money can do.

It’s slow. It’s sneaky. And unless you’re paying attention, you don’t notice it until it’s too late.

Most people think the biggest threat to their money is a market crash. But the real danger is often much quieter. It’s not sudden. It doesn’t come with news alerts. It just quietly erodes your buying power year after year.

Inflation works like background noise. You learn to tune it out. But over time, that noise becomes the reason your rent is higher, your groceries cost more, and your savings don’t stretch as far.

If your money isn’t growing faster than inflation, it’s shrinking in disguise.

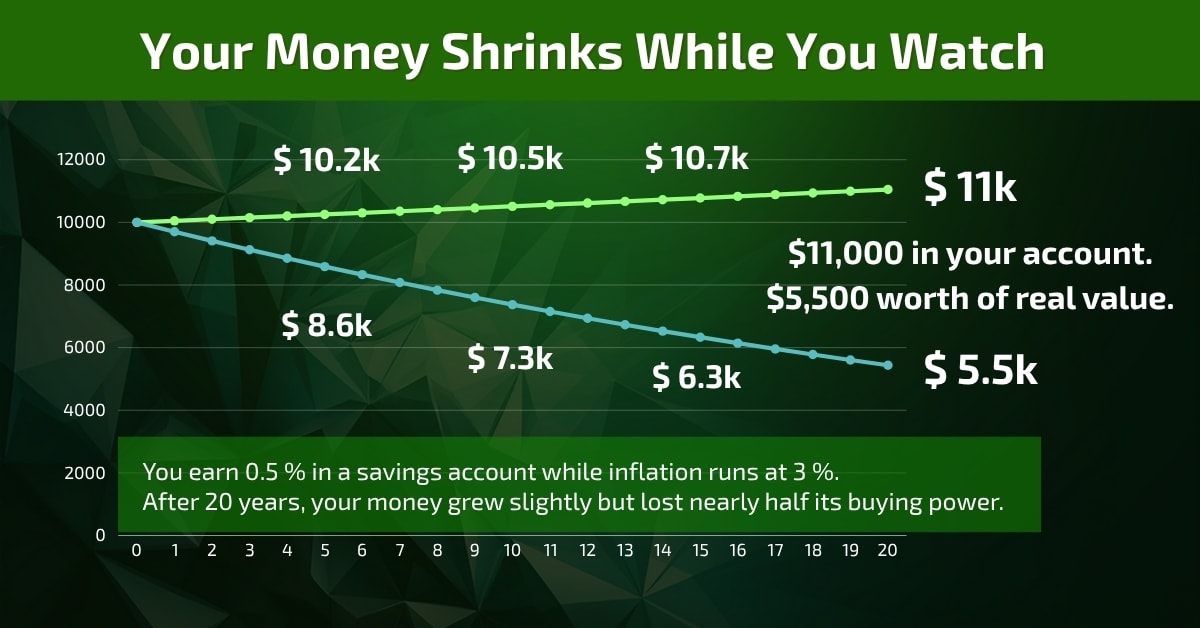

Keeping money in cash or a savings account feels safe. No volatility. No headlines. Just peace of mind.

But that feeling of safety can be misleading. If your account earns 0.5% but inflation runs at 3%, you’re not standing still. You’re sliding backwards. The risk isn’t obvious. There’s no chart showing your loss. But over time, your money quietly loses power. You save more, but you can buy less.

That’s the trap. The most familiar option often carries the most invisible danger. And by the time you notice, it’s already done damage.

Investing in stocks feels risky. Prices go up and down. You see red numbers and panic headlines. But the real question is: risky compared to what?

Yes, stock markets swing. But over the long run, they’ve outpaced inflation by a wide margin. That’s why long-term investors use them to build wealth, not just chase quick gains.

The lesson? Volatility isn’t always risk. And stability isn’t always safe. It all depends on your time horizon and your goal.

Sometimes it makes sense to hold cash. You might need it soon. You might want flexibility. But you should know the cost. That money won’t grow. And if prices rise, it buys less over time.

Good financial choices aren’t just about comfort. They’re about clarity. What are you risking by doing nothing? And is that worth the sense of safety?

The real trick is to be honest about what each option gives you and what it quietly takes away.

Core takeaways:

Next up: See how three everyday investors adjust their strategy to protect their money and keep it growing despite inflation.