Quick Start

Know when to protect and when to grow

Imagine your car breaks down. You need $1,200 today.

But all your money is in stocks. The market is down 12%.

You sell at a loss, miss the rebound, and learn the hard way that investing without a safety net isn’t bold. It’s badly structured. Saving and investing aren’t rivals. They’re teammates with very different jobs.

Savings protects you when life hits hard.

Investing builds wealth over time.

The mistake is treating them the same. That’s when short-term needs collide with long-term strategies and force you into costly moves.

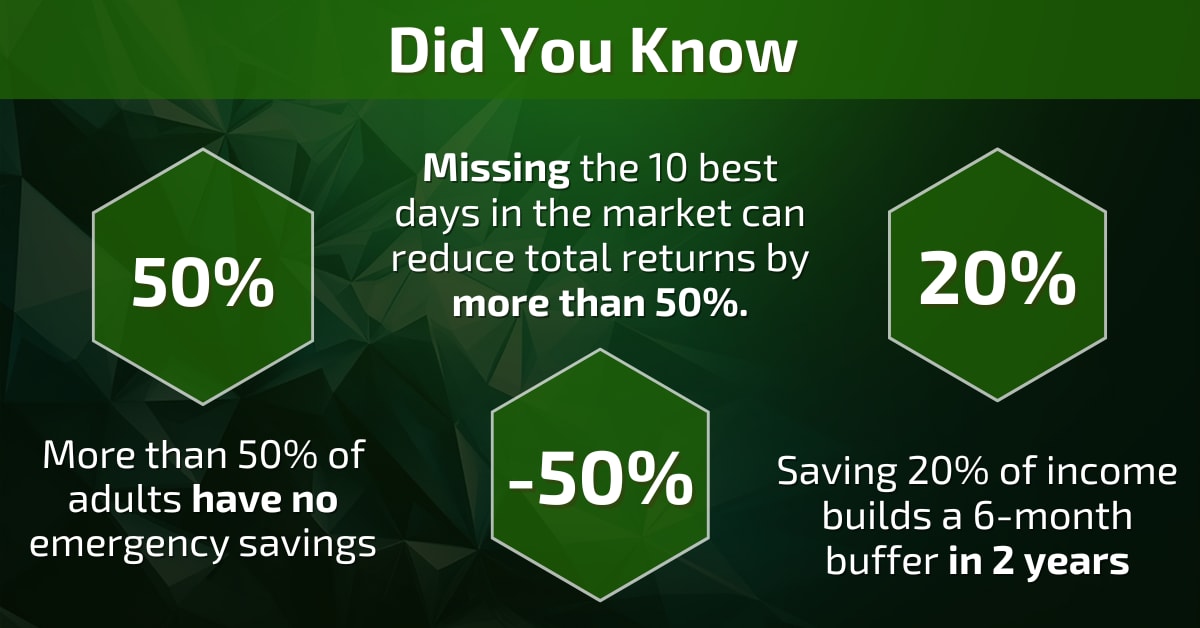

A smart setup starts with a cash buffer. Most experts recommend saving three to six months of essential expenses. That includes rent, food, insurance and minimum debt payments. Not coffee runs or concert tickets.

If your monthly baseline is $2,000, your target savings range is $6,000 to $12,000.

Once your safety net is in place, investing makes sense. But only with money you won’t need soon.

Short-term goals like a new laptop or house down payment belong in savings or low-volatility assets.

Longer-term goals like retirement or financial freedom benefit from stocks, ETFs or crypto. These can swing in the short run but grow in the long run.

One of the most useful guidelines is the 50-30-20 rule. Fifty percent of income goes to needs, thirty to wants, and twenty to saving and investing. That last twenty is where strategy comes in. Early on, use most of it to build your emergency fund. Once that’s done, shift it toward growth.

This isn’t about being conservative. It’s about clarity. Savings keep you steady. Investing moves you forward. When each dollar has a job, you make better decisions under pressure.

Core takeaways:

Next up: See what happens when people get this split right and what goes wrong when they don’t.