Quick Start

Understand the core building blocks of investing

Imagine loading into an RPG and getting random gear with no stats shown.

You don’t know its strength, weaknesses, or when to use it. That’s how many people start investing.

They just grab something called “stock” or “ETF” or something named after a dog and hope for the best.

In reality, these aren’t mysterious acronyms. They’re the core tools you’ll use to grow your wealth.

Each comes with its own potential gains, risks, and ideal use cases. The trick is knowing how they work and how much risk you’re really taking before you “equip” them in your portfolio.

Owning a stock means you own part of a single company. If that company grows, so does your investment. If it tanks, you take the hit directly.

This is where risk & reward become very real.

Single stocks offer high upside, but also sharp drawdowns if expectations break.

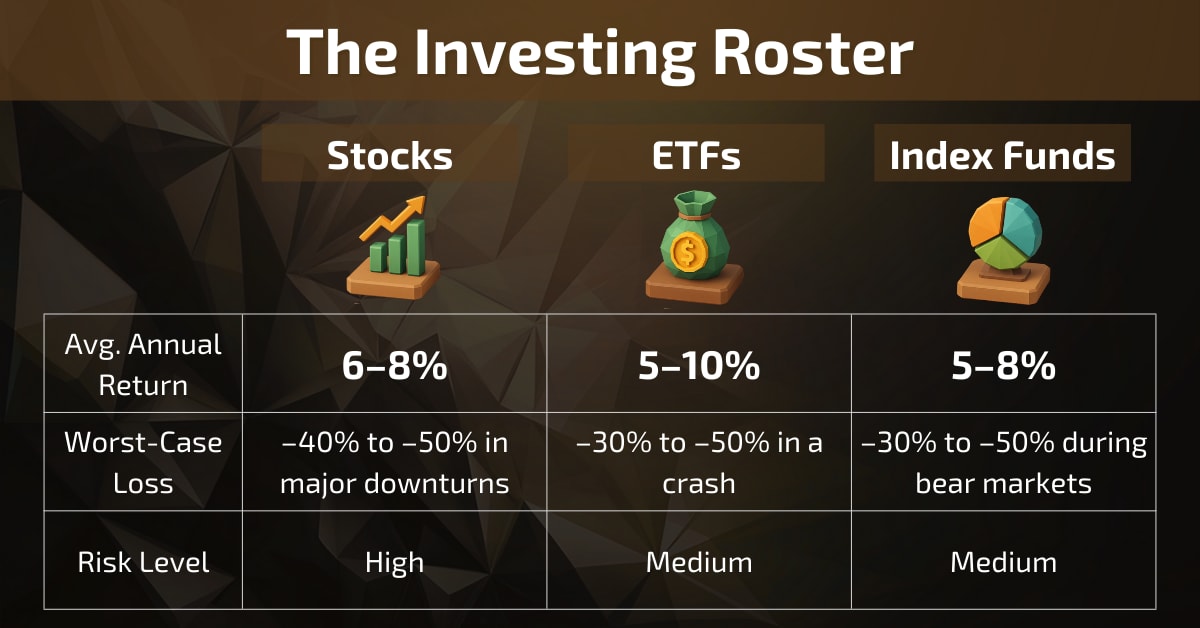

Avg. Annual Return: 6–8% (big, stable companies)

Worst-Case Loss: –40% to –50% in major downturns

Risk Level: High

Pros: High growth potential, possible dividends, direct ownership.

Cons: Volatile, company-specific risk, requires research.

A $10,000 investment in Microsoft in January 2015 would be worth around $64,000 by January 2025 – but during market sell-offs like 2022, it fell over 25% before recovering.

Think of it like running with one powerful hero – huge wins if they level up, but if they get knocked out, your whole run suffers.

An ETF (Exchange-Traded Fund) bundles many stocks, bonds, or other assets into one tradable package. By buying one ETF, you instantly own small pieces of all its holdings.

Avg. Annual Return: 5–10% (broad market ETFs)

Worst-Case Loss: –30% to –50% in a crash

Risk Level: Medium

Pros: Diversification in one trade, lower volatility than single stocks, easy to buy/sell.

Cons: You can’t pick the exact roster, and the mix still moves with the market.

A $10,000 investment in the SPDR S&P 500 ETF (SPY) in January 2015 would be worth about $27,500 by January 2025, with smaller swings than most individual stocks.

It’s like recruiting a balanced squad – tank, healer, DPS – all at once. You spread the risk, but you don’t fully control the team.

ETFs shine when investors want exposure without constant decision-making.

They’re often a core building block in learning how to balance a portfolio.

An index fund tracks a market index, like the S&P 500. It passively mirrors the performance of all companies in that index.

Avg. Annual Return: 5–8% over decades

Worst-Case Loss: –30% to –50% during bear markets

Risk Level: Medium

Pros: Broadest exposure, ultra-low fees, simple to manage.

Cons: No customization – you own the winners and losers in the index.

A $10,000 investment in the Vanguard 500 Index Fund (VFIAX) in January 2015 would be worth roughly $27,800 by January 2025, almost identical to SPY but with even lower ongoing costs.

It’s like joining the biggest guild in the game.

You move with the entire group, for better or worse, without having to lead the raid.

What it means:

Stocks: Highest control and return potential, but also biggest swings.

ETFs: Good balance of risk and reward, easy diversification.

Index Funds: Slow, steady, and cheap – ideal for long-term holding.

In practice, many investors combine all three to balance growth potential with stability.

This is why understanding risk by asset type matters more than chasing returns.

Most investors combine all three using intentional asset allocation instead of guessing.

These aren’t competing products. They’re different tools for different jobs.

Knowing how they behave helps you avoid mismatches between your personality, your goals and your strategy. That’s how portfolios are built on purpose, not by accident.

Core takeaways:

Now that you understand what each asset type brings to the table, it’s time to see what happens when an investor picks the wrong one for their style and how it can derail an otherwise solid plan.